In a recent LES webinar, IP valuation expert and LES Board member, Efrat Kasznik offered a deep dive into one of M&A’s most overlooked complexities: the intangible valuation gap. The session, IP Valuation in Special Situations – Part 1: Closing the Intangible Valuation Gap in M&A Deal Pricing framed mergers and acquisitions as strategic combinations where valuations are shaped not only by financial metrics but also by accounting disclosure—or the lack thereof—of intangible assets. In an interactive touch, she included several polls to gauge attendees’ knowledge. Kasznik was joined by Michael Pierantozzi, LES-SVC Program Chair, who moderated the session, and Stacey Ramsay, LES USA & Canada, who supported the session.

In a recent LES webinar, IP valuation expert and LES Board member, Efrat Kasznik offered a deep dive into one of M&A’s most overlooked complexities: the intangible valuation gap. The session, IP Valuation in Special Situations – Part 1: Closing the Intangible Valuation Gap in M&A Deal Pricing framed mergers and acquisitions as strategic combinations where valuations are shaped not only by financial metrics but also by accounting disclosure—or the lack thereof—of intangible assets. In an interactive touch, she included several polls to gauge attendees’ knowledge. Kasznik was joined by Michael Pierantozzi, LES-SVC Program Chair, who moderated the session, and Stacey Ramsay, LES USA & Canada, who supported the session.

“M & A deals are priced using business valuations, not IP valuations, which do not fully reflect intangible assets.”

— Efrat Kasznik, President, Foresight Valuation Group & LES SVC Chair

M&A Market Trends: Strategic Deals in a Cooling Climate

Kasznik opened with a sweeping look at the state of the M&A market, noting a post-pandemic peak in 2021 followed by a marked downturn through 2024. Despite this decline, Bain & Company estimates a still-robust global M&A market value of $3.5 trillion for 2024, driven largely by strategic buyers. Yet, industry performance has diverged: tech, healthcare, and media sectors have seen steep drops in deal activity, while energy and advanced manufacturing remain relatively strong. Key factors behind the downturn include persistent high-interest rates, increased regulatory scrutiny, geopolitical instability—and, notably, a growing disconnect in how buyers and sellers perceive the value of the deal.

The Intangible Valuation Gap: What’s Missing From the Books

A central theme of the session was the “intangible valuation gap”—the discrepancy between a company’s actual asset value and what’s reported on its balance sheet. Kasznik emphasized that most intangible assets, such as brand equity, patent portfolios, or customer data, are typically absent from standard financial disclosures, which complicates pre-deal valuation. While intangible assets may be identified post-acquisition during the purchase price allocation process, the resulting “goodwill” often obscures the real value of those assets, masking deal pricing inefficiencies.

How We Value Businesses: Limitations of Traditional Approaches

Kasznik walked attendees through the three core business valuation approaches—market, income, and asset-based—each with shortcomings when it comes to capturing intangible value. The market approach, which uses comparable company multiples, is the most commonly applied and often the easiest way to “bake in” intangible value by adding a premium to the multiple. As an example, she cited WeWork, whose valuation multiple of revenue was bolstered by a strong brand and perceived innovation (despite limited IP holdings or R&D investment), as compared with multiples of similar companies in the industry.

Strategies to Close the Gap: Corrective Valuation and Deal Structuring

To bridge the intangible valuation gap, Kasznik introduced two key strategies: (1) valuation correction; and (2) payment engineering. Valuation correction involves adding the non-disclosed intangibles to the valuation of the acquired company by justifying a higher valuation multiple based on intangible assets (such as a unique brand, technology, or data set), or by conducting a separate valuation of intangible assets and adding it to the other assets. The second strategy—payment engineering—includes IP-based earnouts or milestone payments that allow parties to reconcile intangible value over time. These tools enable buyers to assess post-deal performance while offering sellers a pathway to realize value not fully captured in traditional metrics.

Intangible Valuation and Payment Engineering in Action

Kasznik expanded on the concept of corrective valuation strategies by encouraging sellers to either argue for a higher multiple, as previously discussed, or to conduct a thorough valuation of their IP portfolio to justify a higher deal price. One example included a telecom company that used a discounted cash flow (DCF) analysis not only to value its core revenue, but also to project future licensing income embedded in its intangible assets for non-core activities, which provided an additional value to its patent portfolio—resulting in a significantly higher acquisition offer.

She also introduced payment engineering as a creative tool for aligning deal price with IP performance. This includes structuring transactions with IP-based milestones—where the buyer makes payments contingent on achieving specific patent or product development goals. Kasznik emphasized the importance of carefully crafted milestone goals, citing examples of both successful and unsuccessful deals. In one biotech case, poorly defined IP milestones led to a dispute when the granted patents were narrower in scope than expected in the acquisition milestone agreement.

Creative Deal Structuring with IP-Based Payments and Licensing

The webinar also spotlighted the flexibility of IP-based payments, where sellers retain ownership of certain intangible assets and license them back to the buyer as part of the transaction. This model minimizes risk for the buyer while giving the seller an opportunity to generate recurring revenue. A high-profile example was Microsoft’s acquisition of Nokia’s Devices & Services business, where Microsoft agreed to pay ongoing licensing fees for Nokia’s mapping patents (not included in the Devices & Services business) as part of the deal proceeds. Kasznik stressed that this kind of creative deal structuring can add significant value to the seller, and should be considered when intangible assets not included in the deal can be leveraged to offer additional value to the buyer.

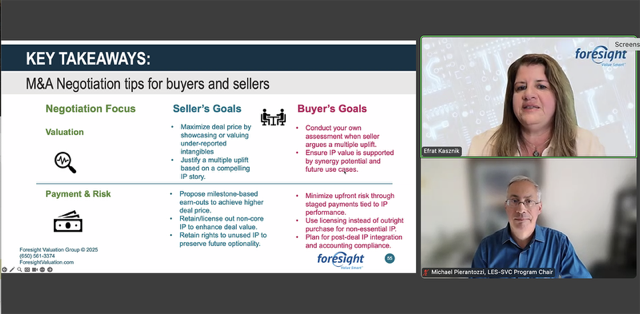

Negotiation Tips: Building Win-Win Deals

Kasznik concluded the session with practical negotiation tips for both sellers and buyers looking to maximize deal value while mitigating risk. Sellers, usually driven by maximizing deal value, should highlight underreported intangibles, justify valuation uplifts with credible IP narratives, and proactively conduct their own IP assessments. Buyers, on the other hand, are looking to mitigate risk, and should be encouraged to verify excess multiples attributed to IP value, and structure deals using earnouts or creative IP-based payments rather than outright payments. At the heart of Kasznik’s message: successful M&A deals are built not just on numbers, but on thoughtful negotiations that create value for both sides.

This webinar and its content are free for members. For access visit:

https://members.lesusacanada.org/general/custom.asp?page=WebinarRecordings

Get Social